I think of Paul Krugman as my favorite Bar Bet Economist. His columns and blogs, which are relentlessly self-congratulatory, seem often (almost always) about a couple of economic parameters which he has gotten right and many of his critics and others have gotten wrong. But these parameters (the coupon rates on Treasury bonds and the overall rate of inflation) are somehow trivial when compared to the enormous economic and environmental problems the U.S. and the other developed countries nevertheless face. Thus, being right on these two indicators is a little bit like the guy on the adjacent bar stool who wants to bet on whether the next car passing in the street will be foreign or domestic, or whether the next woman walking in the bar will be blonde or brunette. Leave me alone, I'm trying to watch the baseball game.

Mr. Krugman says that he has been right not because he's so smart but because his economic model, the Keynes-Hicks IS-LM model, predicted that in a "liquidity trap" such as the United States is in, where monetary policy (essentially, the lowering of interest rates and unconventional quantitative easing by the Federal Reserve) fails to achieve "traction" in the real economy because the American people are already in debt up to their eyeballs. Thus, the central bank (here and in Europe and Japan) is "pushing on a string." Rates can't go any lower, and printing money makes the stock market go up for a while (stock prices are measured in money, after all), but not much else happens, so monetary policy has shot its wad. Mr. Krugman (who actually does think he's right because he's so smart, of course), who is a good Keynesian advocate, thus says that the remaining way for the U.S. economy to "end this depression now" (as the book he's flogging claims) is for the federal government to stop being so "austere" (running only $1.2 trillion budget deficits) and really spend some money. Unlike the deluded "bond vigilantes" and those who have been so wrong about soaring interest rates on Treasuries and inflation (so far) like Peter Schiff, Niall Ferguson and others lacking a deep understanding of the IS-LM model, Mr. Krugman, who has won his bar bets, feels that he is entitled to advance his own theory boldly.

Suppose, however, that something else is really going on these days, something more sinister and threatening that is actually at the root of our economic malaise. Suppose the easy analogies to the ways the U.S. rose from the depths of the Great Depression, or became the world's economic colossus after World War II, are in some ways inapt. Suppose, in other words, it's 2012 now, forty years after the landmark work of the Club of Rome and its Limits to Growth predictions.

Then we really have a problem, because then we're faced with the problems of the real world and not an internecine academic food fight between guys who want to shine at the expense of their peers at the next gathering of other non-scientists spouting (in Feynman's delicious phrase) their "general dopiness," defending their tiny little theoretical turf on which they've staked their academic reputations. Or as Paul Craig Roberts puts it:

"Most intelligent people are aware that natural resources are finite, including the environment’s ability to absorb the wastes or pollution from productive activities (see for example, Jared Diamond, Collapse, 2005). But few economists are aware, because economists assume that man-made capital is a perfect substitute for nature’s capital. This assumption implies that there are no finite environmental limits to infinite economic growth. Lost in such a make-believe world, economists neglect the full cost of production and cannot tell if the value of the increases in GDP are greater or less than the full cost of producing it."

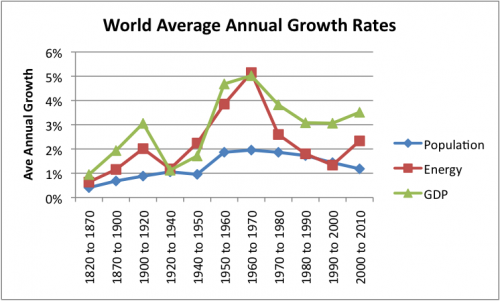

Thus, as Gail notes, the interdependence of GDP growth and energy use, when considered in light of the manifest need to reduce our expenditure of fossil fuels (on the order of 80% between now and 2050, under the most hopeful scenario, in order to keep global warming under 2 degrees C, which may or may not be safe), means that we are in for a very long, protracted period of declining GDP (not growth, but in real terms) between now and 2050, unless we want to guarantee our extinction.

The situation is actually quite syllogistic and not dependent on malarkey like IS-LM Keynes/Hicks Liquidity Trap Zero Lower Bound Monetary Fiscal Mumbo Jumbo, and the rest of the nonsense Krugman and his ilk use for their useless stock in trade. We're at the end of the line, we have to switch over to sustainability and reduced populations, and the Bar Bet Economists have to pay their tabs (which are enormous, because they've really messed up the world with their stupid advice) and go home.